Almost everything is expensive now. Look how much assets in general have gone up: stocks, real estate, collectibles, commodities, and so on. College, healthcare, and insurance too. No reason cars should be an exception.

I was looking at the market charts (NASDAQ) and was floored. How can people look at such a massive increase during a global pandemic and say this is normal growth? I mostly missed out on this entire expansion (we were saving to buy a house; had to keep the downpayment liquid as our housing market is stupid and requires people to go through a dozen bidding wars before you actually succeed).

High demand and low supply due to supply chain slowness doesn't immediately translate to price inflation. Prices go up in this scenario but the question is if it's just temporary (meaning supply eventually meets demand or demand goes away over time) or it is in fact permanent inflation.

Hard agree. Real estate is spiking up, but you are to observe that construction materials and wood just normalized back to where they were. Same with cars, this is due to rental companies repurchasing their fleets. It's a temporary supply issue, we are not in an inflationary market just yet.

Even if brown rice prices were to double, making GABA rice gets the nutrition profile of proper vegetable from a staple.

I wouldn't store the brown rice meant for GABA longer than six months or replace more than half my vegetable intake with it (i.e. one probably shouldn't replace dark leafy greens and/or the broccoli family,) but that is still something like a compensation for 45% inflation in fresh vegetables.

98% of the land that makes up the wheat crop in the US is currently in severe drought. I’ve seen farmers showing land that normally would have wheat 4’ high being 8” high. If wheat fails to this degree, we have a bigger issue on our hands than paying 3-5% more for asparagus.

I was just reading it (on mobile) and thinking that it’s perhaps the easiest to read and clearest article I’ve seen for a very long time. Something to do with the headings and short explanations, the visual layout and the simple but not _too_ simple charts. 10/10 for me - but I don’t need the alt text, so I’m not disagreeing the images should have those, especially as they are important to the flow.

I think I'd prefer web browsers to understand LaTeX, or a similar open and free as in both liberty and beer standard. Maybe SVG for webpages with URI remote resources would be a good alternative, just something else.

I do love simple webpages with minimal resources that don't get in the way of my own preferences and device rendering needs in their quest for pixel perfect publication. HTML and CSS are supposed to be meta-languages that describe to a client how data is structured and simple style elements (that might get over-ridden!).

I would pay a premium for NOT having all the extra electronics --a computer that controls the computer of the computer, a large TV on the dash, a car that only the dealership can fix because they are the only ones who have the equipment to read the codes, everything by wire...I prefer a car that lets me stranded in the road for something I can usually figure out and repair myself, instead of a car that just stops running and has to be towed directly to the dealership for service.

I agree, but also hold an extreme view on the other end. If you’re going to put tech in a car, I want that crap to be Tesla-levels of tech. Not this half-assed 6” “infotainment” crap.

Find a way to slap a straight up automotive grade 23” 144hz touchscreen in there. Or at least do what Tesla did and say screw it and use one that isn’t. Really push the envelope or don’t bother at all.

I expect more from BMW, Daimler and Volkswagen but they produce absolute garbage. Audi owner here.

Objectively just about everything is abnormally expensive right now. Not just in the USA, but also Canada and Australia that I know of. Maybe other places as well.

Adding to the remark in the article about new and used cars being linked at the dealers: many new car dealers do not shop at auctions. They only buy used trade-ins partly to help encourage new car purchases ie the "four square" calculation they use.

So when their new car supply is interrupted upstream, that also interrupts their flow of used cars, so some dealer lots are a little thin on both new and used inventory at the moment.

The Kia Telluride is selling for quite a bit more than MSRP, used. Apparently dealerships are asking for more than MSRP new and that is part of it (in addition to/because of low availability)

The thing I find oddest about that, is I always hear about the Telluride, but the Hyundai Palisade rarely comes up. I couldn't figure how they could differ enough to cause such a disparity. I assume in reality, Palisade pricing has to be similar, right?

Now I say that, but I also think I can answer my own question.

Mainly, I would say I'm hilariously confused by how Hyundai positions Kia and Hyundai. Like on paper it I thought that Kia is supposed to be the sportier one, and Hyundai (nominally) luxury.

But when I was shopping, both had really confusing trim levels, and Hyundai was especially odd because you really had to trim up to get what I would call a luxury car, leather upholstery was the big one.

The marketing seemed to try and paint Hyundai as like refined style, but the actual car features of the two brands just made me hella confused.

I think it's safe to say Hyundai/Kia made a lot of strides, they could use some work there.

My suspicion is that Kia/Hyundai's current marketing position is about capturing new car purchasers, not differentiating brands.

Your average consumer will only drive a few cars before buying one, 3-5 maybe? So if you can own two of those slots with cars that are practically the same but somewhat different, you increase the chances that a consumer will buy one of your products because they are less likely to look at competitor's products.

Curious what others think on this. Seems like a smart business strategy.

They have been saying that since the car released. Kia has been playing NY nightclub bouncer with the availability and enjoying the extra $$ they get on top.

Of note drive an Optima so not a super Kia hater just what they have done with the release of this model

Now's the time to sell a car if you have an extra to spare. One of the few times in history when cars actually appreciate. A car I bought for 53k 4 years ago I could've sold for 55k last week until I got cold feet. lol

I’ve had folks who found out I’m about to take delivery of a Model Y offer me ~$10k over list if they can buy it immediately after I take delivery. It’s insane.

Know a guys who just sold his Tesla to a dealer for $50k. Same price he paid. He owned for for 2 years and suffered $0 depreciation. Replaced with a cheaper car.

Haha. Mine is a Model S. It's my baby so of course I couldn't sell it. I had just posted it for shits and giggles at a ridiculous price but I guess people are desperate.

I'll sell it once my Cybertruck preorder is ready! haha`

I just noticed a '86 toyota truck on CL going with an asking price of $28,000.00

I noticed it because I like their trucks, especially the 22r/re ones.

It did have less than 30,000 miles though.

The price of that truck is no more than 5 grand, even with the low miles.

(Anyone looking for a ride, I have this tip. When four door vehicles are aging out of what Uber demands, they price of the used vechicle goes way down. Look for vechicles that have aged out of the app, or close to it.)

I think small Toyota trucks are drifting towards some kind collectors status.

A few years ago I sold a gen 1 Tacoma for nearly double what I paid, only because someone tipped me off that the price was high for that model on Craigslist.

Small, lightweight pickups are no longer being manufactured. And Toyota’s are ridiculously reliable. My old truck still ran like new with nothing but regular oil changes and a one-time replacement of the spark plugs.

Ever since the frame recall, the prices have been ludicrous for Tacomas. 1G with the 2/3RZ engines will run forever with little-no maintenance-- multiple people in my family have ones approaching 400k miles. They're utilitarian, rough ride quality, noisy-- but they're trucks (& can get 27mpg highway). Unfortunately, Toyota has kept moving further upmarket and keeps making larger & larger trucks (a $60k Tacoma?) that aren't really as appealing as 4/5th gen pickups or 1g Tacomas.

Around the mid 2000's, something seems to have changed with Toyota-- maybe more emphasis on design & listening to what fat Americans want (wider seats, heavier duty suspensions, more ground clearance to go to Starbucks) vs building high quality functional vehicles. They're still better than others, but it seems that they've had more issues with quality, at least in the models that I've researched.

Those trucks rust like crazy if they are driven where salt is used in the winter. I owned an 87 Toyota truck and it perforated with rust by the mid 1990s.

If you're in California or southern US they probably last a lot longer. The 22RE engine is very good.

Just did and got a good price. The only problem is I'll probably need to buy another once Covid calms down and we go back to work. I'm going to try to use public transit and cycling for a bit, but the reality is I'll need to get another car within a year. Hopefully someone has a small, cheap electric by then.

Stocks are vastly superior to real-estate. Businesses with reliable growth and some pricing power.

The S&P500 has generated approximately a 266% return in the past 20 years (ex any dividends). The average home sale price has climbed by just under 100% in that time.

Real-estate will nail you annually on property taxes (although not in every state) and you have to maintain it (let's assume a best case and you own it without a mortgage).

You can sit on a stock you bought for a decade, not sell it, let it appreciate by a lot, and incur zero taxes on the holding the entire time.

The average US house incurs ~$2,500 in property taxes each year (a painful expense across a decade). And you have to out that cash every year. If for any reason you can't come up with the taxes, they seize your property; that doesn't happen with a stock holding. The government doesn't care if the real-estate is going up in value or not, they want their property taxes. At least if your equities don't go up, you owe nothing when you sell. Equity trades also have zero commission now in most cases - you can sell a million dollars worth of stock at zero commission; you can't do anything remotely like that in most cases with real-estate.

Most real-estate struggles just to keep up with inflation. Average home sale prices haven't managed to outrun the cost inflation in average new car sales in the past 20 years. You're probably as well off sitting on gold ETFs like GLD or IAU as you are typical real-estate as an inflation hedge (IAU only has a 0.25% management fee, far lower than the typical real-estate property tax).

In most states your real-estate will also suffer a persistently climbing tax basis if you're lucky enough to see value gains; and local governments love to increase property taxes whenever they can.

And last but not least, in most cases you can click a button and liquidate your stock holdings in a matter of seconds or minutes with near zero hassle.

Obviously that equation changes if you're an experienced, competent property manager and you can get a healthy yield from your real-estate; however that's a serious job, with an enormous time/effort/labor/legal/mental burden, not a low-effort side task (much less a near zero effort task like sitting on the S&P index).

I used to think this way and realized there were two key things I missed (these are game changers).

1) There are places where the appreciation on the primary residence is not-taxed or taxed at a low rate. I.e. In HCOL areas, people who just bought a house and did nothing much in life (say, drove an Uber just to make ends meet), are worth 1-2 million dollars after tax.

2) When you buy real-estate through a mortgage, you are getting massive leverage on your investment. Would I borrow 5x my principal to buy shares? No! Why is that? If prices go down on shares and I bought on margin, I can get a margin call. If I have a 25-30 year mortgage, I can ride the ups and downs.

These are all my personal experiences .. I followed blogs like greaterfool and totally missed out on some key aspects in life. Owning a home was a much more pleasant life experience than renting for me personally. It is certainly more risky (with respect to restricting job mobility), and more expensive in some respects (utilities). I just want to provide a counterpoint to your argument. Not a financial advisor so pls don't take stock in anything I say :)

A few issues with your two points, I think, are that real estate values don't always go up forever, even in hcol areas. It's not always evident what areas are about to have years and years of high growth.

Now, buying a home for your own personal use and as an investment is a better proposition. But you can only have one of those and you can't get such low interest rates and low money down for investment properties as you can for a personal home mortgage.

Regarding S&P 500 vs. real estate returns, you are assuming someone buys a home with 0% leverage, but most people use leverage via a mortgage, which boosts returns both from price appreciation and rent. Also, locking in a low rate is a great inflation hedge. Also, real estate is not as highly correlated with the market, so it has benefits from a diversification standpoint.

This is not quite correct. In high inflation credit markets disappear. 80%+ of housing is bought on mortgages. If 80% of housing demand disappears you get a 2008.

The 2008 global financial crisis was due to a compete failure of risk management in originating mortgages and packaging them as mortgage backed securities. In short, the industry was scraping the barrel and shoveling shit to investors. “If they can fog a mirror, fund the loan” was a phrase common at Countrywide. Lending standards are comparatively tight now, no NINJA loans [1]. The credit market will tighten, but housing demand won’t evaporate, and investors are starved for yield.

In high inflation environments, you want to lever up with debt to fund investments because your debt will be inflated away over time while you capture cash flow or asset appreciation. High yield debt (“junk bonds”) are also a great play for such a macro environment.

Your debt gets inflated away gradually while your asset crashes today. If housing went down 30%, virtually all debt in housing sold in the last few years would be underwater, which tends to increase delinquency ("they can take the house back"), which then makes the bank eat that loss and having toxic assets.

It doesn’t matter if it’s underwater as long as the debt can be serviced. That’s the difference between a margin loan and a mortgage; there is no margin call on a mortgage. It can lose 99% of its value and as long as you still make payments (or your tenants so), you continue to own/control the asset.

In certain circumstances, absolutely (if rent payments would be higher than the mortgage payments over the holding period, or if the value of the property would accelerate past the mortgage balance during the holding period).

Interesting counterpoint .. you are right .. why would I lend you a dollar if I expect it to be worth a lot less in the future. Any data to go with this assertion? In Canada, average mortgages are just for 5 years - this is very different than the US. I suspect banks are taking very little risk in such a scheme. In the US, I believe banks sell mortgages off/get insurance via govt. schemes.

I think it was because people freaked out on public transit. In fact, there is a run on getting licensed to drive (have multiple co-workers trying to book appointments; they used to rely on public transit but realized it was suboptimal during covid). I recall it was very expensive to buy a bicycle in my city this time last year (those had a dual purpose - exercise/outdoors + transit).

Cash is being pumped into our economy, therefore, people want to buy more stuff, because now they can "afford it."

So now with more competition for goods and services, prices go up because there is more money than there are goods and services. I work with businesses in the trades (auto repair, plumbers, HVAC, insulation, etc) and they are all at full throttle, and cannot handle any more work. So those companies are going to start raising their prices. But this happens in all areas of products and services. There's just not enough stuff.

As a result, there's inflation. Inflation is the decline of purchasing power of a given currency over time. I lived through the 1980s, where there was an inflation rate of 16 to 18%. This means, let's say you have $10,000 in the bank, in 1 year, the purchasing power is $8,200. The next year it will have the purchasing power of $6,724. The third year your original $10,000 will be worth $5,513. Your bank account will still be $10,000, it's just that you'll only be able to buy $5,513 worth of products and services, on the average.

The way to protect oneself is to buy stuff, and not keep any cash in the bank account. If you purchase $10,000 worth of canned food today, the value of it will remain the same over time, because you purchased, oh, let's say 10,000 cans of food, but in 3 years, you would only be able to buy 5,513 cans of food. So you get rid of cash as fast as you can. But instead of buying food, which you might do, you also buy houses, cars, anything. Because those things, when you sell them, will be the same price. If a can of peas goes from $1 to $3 over 3 years, you can sell your 10,000 cans of food for $30,000, if you could, so you still have the same amount of purchasing power. It's not the worth of the things that changed, it is the worth of the money to buy the things decreases.

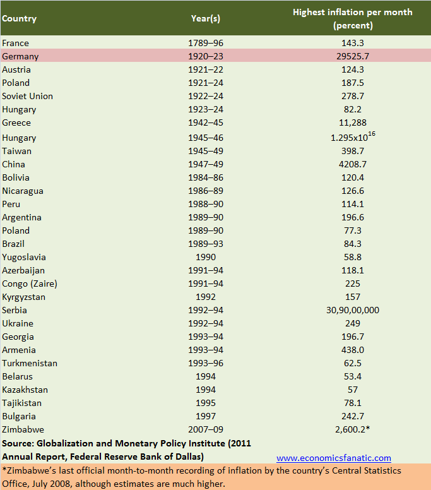

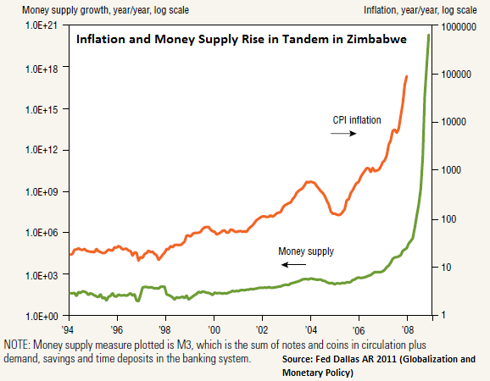

This is well-known, so people with a lot of money are buying second houses or anything else to get rid of cash. So the world is awash in cash, but runs out of stuff to sell, and prices go up. It is a vicious circle, and keeps spiraling out of control, and eventually you can get into hyperinflation, where you can have $1 trillion dollars to buy a loaf of bread. Here is a list of countries that have experienced hyperinflation: https://static.seekingalpha.com/uploads/2012/7/14/426795-134... Most recently, Zimbabwe had hyperinflation and here look at the money supply: https://static.seekingalpha.com/uploads/2012/7/14/426795-134... They just started printing more and more money, until it got out of control.

In Venezuela in 2016, inflation reached 1,000,000%. This means that if it took $1 to buy a loaf of bread in 2015, a loaf of bread would cost $1,000,000 in 2016. And so, the government would be forced to print $1,000,000 bills. In April 2019, the International Monetary Fund estimated that inflation would reach 10,000,000% by the end of 2019. Here is a real 50 trillion bank note from Zimbabwe due to their hyperinflation: https://cdn.shopify.com/s/files/1/0251/2392/products/zimbabw...

This is the exact same thing the USA is doing with unemployment benefits, and people make as much or more than in their jobs, and they don't have to pay rent at all, so all that money goes into all kinds of stuff. The USA is effectively printing up money.

Will the USA end up like Zimbabwe? Almost guaranteed not to, as we have a lot stronger economy, but no one knows the future with certainty.

Zimbabwe? Probably not, but I think something similar to Argentina (it is not unusual to see credit card offers with 100%+ interest). We won’t see 1,000x inflation but strojg inflation could be in the cards, especially if we keep expanding the money supply.

Eventually something has to give.

Yes, I agree. I was just trying to give an overall feel of the situation, rather than the specifics. I added specifics to help understand, but whether or not it is exact is not really my point, it was to give a 35,000 foot view, while looking at a tree or two in general.

Unlike the 70's it's not a single thing that had had upsets but multiple things in countless pipelines, increasing the cost and difficulty of getting workers, materials, and transportation.

I'm guessing logistics are all screwy in dozens of areas and prices are rising as fast as they can while capitalistic opportunists are trying to "get theirs" in the melee.

New cars are not nearly as inflated. The answer to the first question is yes, it's a very good time to sell old and buy new. One stipulation is that ordering a new vehicle with specifications they don't have on the lot will take in the realm of 6 months. Pretty big trade off, but I'm about to deal with this myself and can afford the time difference.

you certainly won't be finding a deal new. friend of mine's father owns a group of dealerships in the town, they have people going to other dealers paying MSRP just to have inventory on their lots and sell for more obviously

Inflation and the fact that new cars are super hard to come by. I just bought a new truck, I was able to get the allocation as I have a friend at the dealer. I got the only allocation they were getting this summer, and I’ve been waiting since March.

The semiconductor fabs didn't shut down last year, did they? If we've run out of so many chips, there must be a glut of some other chips that nobody wants?

Are distributors holding zillions of unsellable obscure level shifters or CPLDs or something?

Probably the fabs that made these chips haven't made them for years. They probably cranked out billions of them 20 years ago then converted to producing something more valuable.

We've probably run out of new old stock and nobody wants to go back to making these cheap chips.

I haven't noticed a major increase in used motorcycles, but your mileage may vary based on region. I'm in Socal. I don't think motorcycles are as complicated or chip based to manufacture and motorcycles are mostly a luxury item in the US. You'll be fine!

Both used and new motorcycle markets are incredibly tight, at least in California where I have been looking. I went to the Honda/Yamaha dealer in Berkeley and quite seriously there were no bikes on the floor. Literally none. It looks from their website that they have a handful now, but none of the stuff they would normally try to have in inventory, like the Honda NC750, XR650L, CRF300L or other dual sports, so sports or supersports bikes, no Gold Wings.

tl;dr of the article is that the pandemic caused a major hiccup in the new-car pipeline: first people halted buying, that caused manufacturing to pause. Even when the manufacturing started again, the chip shortage came in.

In general, it seems people started being more frugal and smarter with their money: people bought fewer new cards and people had few repos. Of course, what makes a car "used" is time, so fewer new cards last year also means fewer late-model used cards this year. Increased demand and decreased supply.

All in all, I think it's a major correction of the prices of used cards. It never made much sense that a new car had half its value fall off when you drive it off the lot, but it was just an accepted fact and a reality (as all value is determined by what's agreed up on explicitly or implicitly).

From what I'm seeing in relatively extensive research lately, the KBB doesn't seem to reflect the difference much, especially for trade-ins. It could be that dealers aren't willing to put up with the inflated prices for trade-ins, but either way you're almost guaranteed to get a hefty bit more selling privately.

I like that everyone readily understands the supply/demand phenomenon as it relates to the price of used cars, but many people are unable or unwilling to grasp the relationship between the supply of new houses and the prices of used houses.

Zoning which prohibits or heavily restricts multi-unit housing in cities, and material shortages and high prices for steel and lumber which impacts new single family homes.

That's a minor factor. It does not explain how this situation happens all over the world, even where there is no overzealous zoning or high prices of materials.

The issue is cheap credit and the lack of an LVT that would avoid all the economical and ethical issues with land ownership.

I don't know how your can say that an LVT avoids all economic and ethical issues with land ownership, that seems like a personal moral opinion. Especially since there's very few instances of an LVT on the wild. I'm sympathetic to Georgism, but you're making a very powerful and unsubstantiated claim.

You're right, I didn't mean "all", I meant "some".

I don't think it's a panacea at all, I just think it would be the most effect with the smallest disruption (in that it's simply a reform to be done inside the framework of free market, private property, etc).

Zoning and Price of Raw goods. For awhile lumber prices alone added an additional 15-30K to the cost of building a new home.

This caused the builder to focus on building more higher end homes, so new homes in the 5-6x median income market were being built but the home in the 2-3x median income home that most people would buy (and should buy) was not cost feasible to build.

We could discuss and debate the various reasons, but at least we'd have a shared basis for understanding the issue. There are other people who say that up is down, war is peace, and that producing new houses somehow also raises the price of houses!

Cheap money. Low lending rates are driving people to buy new (to them) houses. You'll also find unprecedented demand for renovations as people take cash out with refinances to fund their improvements.

Make an actual argument. Are you saying that the legislation reduced the level of housing created? Are you saying that redlining increased housing stock? Are you saying that black people having equal access to credit made white people less likely to build houses?

Linking to Wikipedia with a wink and a nod to racism is not an argument. Be explicit with your argument here.

There was an entire system built around keeping certain people out of many homes and many jobs as possible. When those things became unlawful, do you think the people responsible for the old system would immediately change their mind about the whole thing and give it up, or do you think they would find esoteric ways to maintain the same effect? Do you think they would admit it if they did? Learn to read between the lines of the world around you.

You can't make more land, but you can increase density by putting more units on the same plot of land. This is a totally natural way for cities to develop, but it's more or less illegal in the United States due to zoning.

There's plenty of new land in America and most countries. It's unused because it's far away from where people currently want to be, but that could change depending on what society and industry needs. Maybe remote work will somehow really last and push people out of cities so they can buy an otherwise empty section of wasteland.

Even within cities, it can be creates by zoning changes. My city recently relaxed density rules, effectively creating new land out of nothing in an instant. Developers are now building on that "new" land.

I think there are another two reasons not mentioned in the article. One is the surge in electric car sales, many people are still on the fence and want to wait a year or two before they decide if they want to move to an electric car. That's why they don't sell their own car yet.

The other reason is that in a certain time during the last 20 years there was a sweet sport of car reliability when cars were not too sophisticated but also got rid of all their childhood deficiencies and they can simply go forever. All those corollas and their ilk are just there and not going anywhere so people has no reason to buy new cars instead of those.

{kind=link}

{kind=link}

{kind=link}

{kind=link}